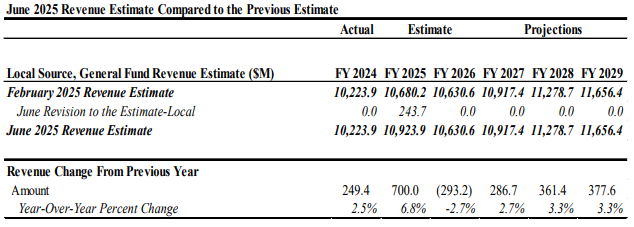

The District of Columbia’s June revenue estimate raised the FY 2025 forecast by $243.7 million, following an unexpected surge in April tax payments from corporations and high-income individuals—an "April Surprise" driven by strong capital gains and profits related to tax year 2024. As this boost is considered one-time in nature and the broader economic outlook has not shifted since February, projections for FY 2026 through FY 2029 remain unchanged. While year-to-date collections remain robust across most major tax categories, economic uncertainty due to unresolved federal workforce policies, shifting trade and immigration rules, and the broader risk of national economic disruptions continue to pose risks to the outlook.

Below is the letter our office sent to the Mayor and DC Council, outlining our June 2025 revenue estimate. Read the full letter with data appendices here. Read the PowerPoint overview here.

This letter certifies that the revenue estimate for the FY 2026 – FY 2029 Budget and Financial Plan of the District of Columbia remains unchanged from the February 2025 estimate. FY 2025 revenue has been revised upward by $243.7 million based on year-to-date collection data, which shows substantially higher-than-expected corporate and non-withholding individual income tax revenue. The increase in individual income and corporate tax revenue is due to capital gains from high-wealth individuals and unexpectedly high profits and foreign income from major corporations, as revealed in April tax filings. Most of the additional revenue in FY 2025 is nonrecurring, as it is based on exceptionally strong income and asset price appreciation from last year, which is not expected to be repeated in the current economic environment.

The economic outlook for the District remains mostly unchanged since February, although the level of uncertainty has grown. Legal challenges to many of the federal workforce reductions proposed by the current administration have added to the uncertainty regarding the timing and extent of those reductions. Shifting federal budget, trade, and immigration policies further increase economic uncertainty. The U.S. Bureau of Labor Statistics revised downward the employment figures for the District for FY 2023 and 2024, but increased estimates for resident employment and the labor force. Additionally, the U.S. Bureau of Economic Analysis lowered personal income and wage estimates for the fourth quarter of FY 2024, resulting in a revised, lower growth forecast for FY 2025. These adjustments were already factored into withholding income tax receipts, which align with the February forecast. Given no major changes to the economic outlook aside from heightened uncertainty, we are maintaining the February 2025 economic forecast with only minor adjustments for updated historical data.

This estimate is based on various sources, including cash collection reports; federal data on District population, employment, and income; private sources on housing, commercial real estate, and hotels; economic forecasts for the U.S. prepared by the Congressional Budget Office and private-sector economists, such as the Blue Chip consensus forecast by 50 private-sector economists and two private firms (S&P Global and Moody’s Analytics) that also forecast the District’s economy.

FY 2025 Revenue Highlights

Year-to-date revenue data show collections are 9.9 percent higher than the same period in FY 2024. A portion of the additional revenue is due to a policy change which increased the rate of Paid Family Leave (PFL) employment taxes which were then transferred to the Local fund. Individual income tax revenues increased by 13.4 percent year-to-date, driven mainly by the non-withholding component, particularly final and extension payments. As noted earlier, greater-than-anticipated final and extension payments significantly contributed to the strong year-to-date tax revenue performance, in line with trends in other states and the nation. The withholding component of individual income tax rose 8.1 percent through March, above the February forecast of 4 percent. Since then, receipts have declined by an average of 0.3 percent each month. As a result, withholding income tax revenue is expected to meet the forecast by the end of the fiscal year.

General sales tax revenue has risen by 5 percent, surpassing the February forecast of 2.2 percent, mainly due to higher tax receipts from restaurant and hotel taxes. As a result, the estimate for general sales tax revenue in FY 2025 has been increased by approximately $28 million to reflect stronger-than-expected year-to-date cash collections. The recent downward trend in hotel sector tax receipts raises concerns and is expected to slow the overall growth for the fiscal year.

Real property tax receipts declined by 1.1 percent based on first-half collections, which is better than the forecasted decline of 2.6 percent for the fiscal year. Real property tax receipts are expected to meet the annual forecast with the second-half collections. Real property tax refunds have already increased significantly—up 96.5 percent this year—adding some uncertainty to the forecast.

Local non-tax revenue grew by 27.9 percent year-to-date, almost matching the forecasted 28 percent for the fiscal year. Most of the growth was driven by additional employer contributions to the Universal Paid Leave Fund, which were transferred to the Local fund per the Universal Paid Leave Amendment Act of 2024 (already reflected in the February forecast). Declines in automated traffic enforcement, business licenses, building permits, motor vehicle registrations, and lottery sales pose a risk that total non-tax revenue may fall short of expectations by the end of the fiscal year.

Year-to-date revenue growth remains strong, but it is important to remember that the uncertain economic environment poses significant risks to the revenue forecast. The direct and indirect effects of federal workforce reductions, as well as changing federal budget, tariff, and immigration policies, could undermine the current revenue strengths. These risks are discussed more fully below.

Risks to the Economic Outlook and Revenue Forecast

The current forecast carries several notable risks. As a government-dependent economy, the District relies heavily on federal jobs and related economic activities, making the new administration's policies a key factor in shaping the city's economic outlook. If the administration’s proposed workforce reductions are upheld by the Courts or are sustained by Congress in the Fiscal Year 2026 federal budget, the economic impact on the District will be substantial. In either case, layoffs of federal employees could happen more quickly and be on a larger scale than currently expected. Although the private sector might absorb some displaced federal workers, the recent slowdown in the local job market leaves limited room for substantial private sector growth.

Shifting federal budget, trade, and immigration policies create considerable uncertainty for businesses and consumers. Changes to tax laws and discretionary spending could either benefit or harm the District's economy and finances. Stricter trade and immigration policies might disrupt supply chains, raise input costs, and slow population and labor force growth, potentially reducing economic activity in the District. Other national risks include recession or stagflation (a mix of slow growth and high inflation), along with escalating conflicts in Ukraine and the Middle East that could disrupt energy markets and trade flows, and potentially reshape fiscal priorities.

The growing volume of vacant office space remains a major concern. The average vacancy rate for office buildings in the central business district was 16.9 percent in the first quarter of 2025, slightly below what it was at the same time last year but higher than it has been in decades. A recent study by the D.C. Office of Revenue Analysis revealed that between 2020 and 2023, vacant office space increased by 8.4 million square feet, a 46.2 percent rise, primarily driven by the shift toward remote work. This trend is expected to continue for at least the next few years, even with the recent return-to-office order for federal employees. The assessed values of hundreds of office buildings are projected to remain depressed through 2029. A sharper-than anticipated decline in property values could pose a risk to commercial property and deed tax revenues.

The prevailing risks and high level of uncertainty create a challenging forecast environment. We will continue to carefully monitor monthly revenue collections, progress on federal budget deliberations and federal employment, developments in the nation's economy and capital markets, and any geopolitical events that could impact the forecast.