The District has two tax credits for individuals and families with childcare costs: the DC Child and Dependent Care Tax Credit (CDCTC) and the Keep Child Care Affordable tax credit. This post will summarize the total tax benefits received by District tax filers under the DC CDCTC and how those numbers changed for 2021 as a result of the federal American Rescue Plan Act (P.L. 117-2).

The DC CDCTC is tied to the federal CDCTC. In order to be eligible for the federal CDCTC, a taxpayer must incur childcare expenses during the year for one or more qualifying individuals, such as a child under the age of 13 or a spouse or dependent who requires full-time care. The maximum qualifying childcare costs are $3,000 for one qualifying individual and $6,000 for two or more qualifying individuals. The federal credit percentage is between 20% and 35% of these qualifying costs.

While the federal credit percentage can reach up to 35% for filers with less than $15,000 in income, these filers often do not actually benefit from the credit. This is because the credit is nonrefundable, which means that the credit amount cannot exceed the amount of the filer's income tax liability. As a result, these taxpayers are not able to take full advantage of the credit.

The federal credit percentage phases down from 35% to 20% for filers earning over $43,000. For filers making more than $43,000, the maximum federal credit is $600 for one qualifying child and $1,200 for 2 or more qualifying children. There is no income phase-out.

The DC CDCTC is a nonrefundable tax credit equal to 35% of the federal CDCTC. For filers earning over $43,000 the maximum DC CDCTC is $210 for one qualifying child and $420 for 2 or more qualifying children.

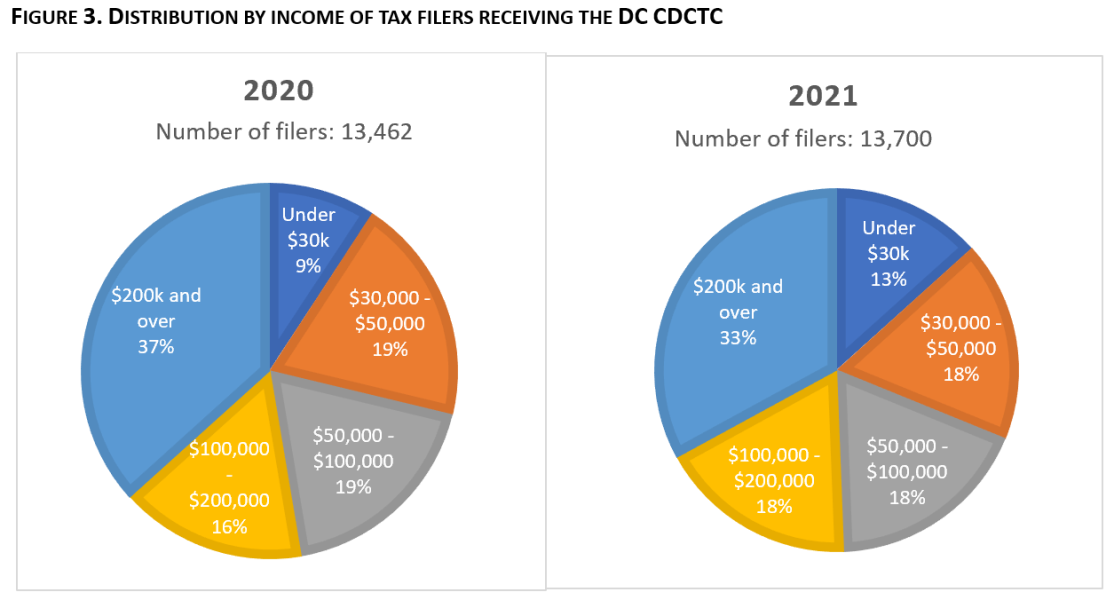

In 2020, 13,462 filers claimed the District CDCTC, for a total of $2.5M. Just less than half of all claimants had an adjusted gross income of $100,000 or less. The average DC credit amount was $185 per filer.

Federal changes to the CDCTC in tax year 2021

The federal CDCTC was substantially expanded for tax year 2021 in the American Rescue Plan Act. Specifically,

1. the credit was fully refundable at all income levels;

2. the cap on childcare expenses was raised from $3,000 to $8,000 for one child, and from $6,000 to $16,000 for more than one qualifying child;

3. there was a higher credit rate for low- and middle-income taxpayers; and

4. the credit is phased out for taxpayers with income of $400,000 or more.

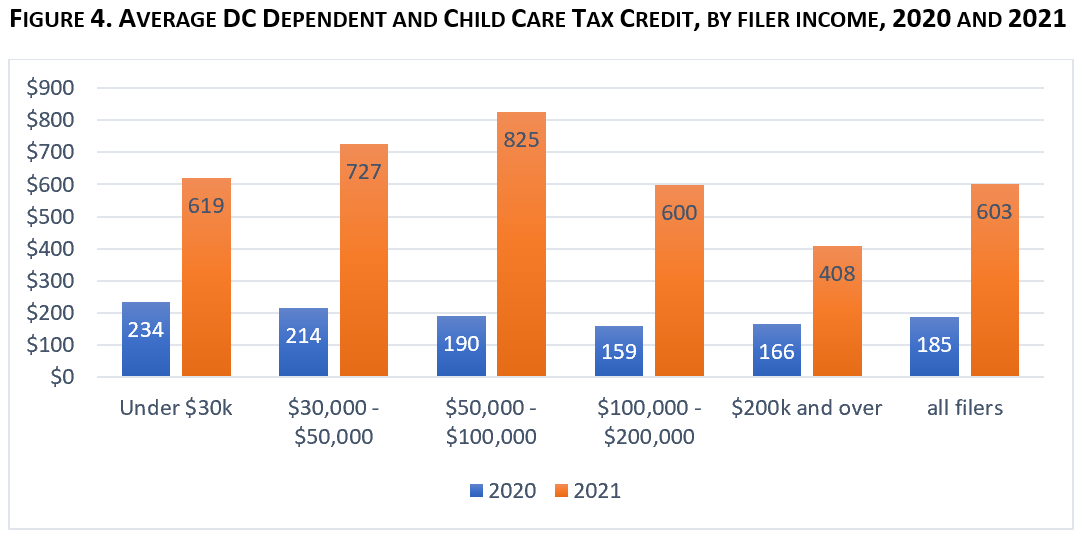

Because the DC credit is tied to the federal credit in amounts and phase-outs, these changes flowed through to the DC credit. While roughly the same number of filers claimed the DC CDCTC in 2021, total credits were $8.258M (up from $2.5M in 2020).

Average per-filer credits increased across all income categories, more than tripling on average from $185 to $603. Higher gains accrued to filers with income between $30k and $100k.

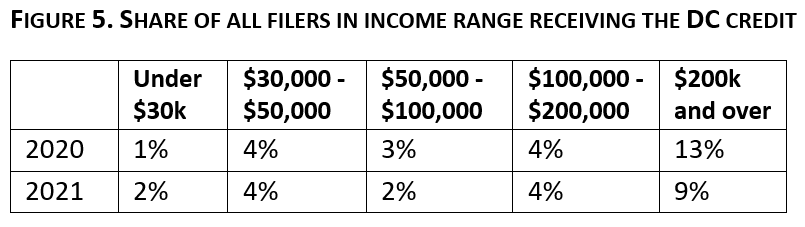

Consistent with provisions increasing the credit amount and qualifying childcare costs and establishing an income phase-out for the highest-earning households, the share of all District tax filers claiming the DC credit increased slightly for the lowest-income households and decreased for the highest-income households.

The CDCTC expansion applies only for 2021, and the CDCTC thresholds will revert to the 2020 levels for tax year 2022. In other words, in 2022 and later total spending will be lower, the credit amount will be smaller, and the distribution of credits across families and individuals by income will look more like the distribution in 2020 and prior years.

Because the DC CDCTC is tied explicitly to the federal credit, changes to federal provisions defining the amount of qualifying costs, credit percentage, and income phase-outs flow directly to the District credit, increasing District spending.

Conformity between federal and District tax policy

The District’s income tax code conforms to the federal tax code in its definitions and rules to simplify filing and administration for District residents, unless District lawmakers have passed legislation to specify different treatment. Conforming the tax systems can help relieve the burden of updating every provision in the tax code every year and minimize the risk of gaps or notches in tax credits and incentives. DC’s individual income tax code also automatically incorporates changes to federal individual income tax policy (a practice called “rolling conformity”). For example, if there is a federal change to a tax concept used in both federal and District law, it will flow through to District income tax law.

DC’s CDCTC exemplifies one downside of rolling conformity. Changes made to the federal credit caused the cost of the program in DC to increase more than threefold, from $2.5 million to $8.3 million. Those changes occurred as a result of federal law, not District law. Yet spending for the DC credit increased.

Intuitively, rolling conformity magnifies the effect of federal tax policy changes on District residents. Federal changes to income tax law in the future—either active (such as tax cuts or increases) or passive (such as the expiration of temporary policies) will flow through DC’s tax code and affect the District’s revenue as well as the taxes paid by, and credits available to, District residents.

What exactly is this data?

You can download some of the data we used for this post here [DC Statistics of Income (SOI) | ora-cfo]. Below we describe how we gathered the data.

The Office of the Chief Financial Officer releases the District of Columbia Statistics of Income (DC SOI) summarizing individual income tax collections for taxpayers in the District of Columbia. This brief uses these publicly available tax data from 2020 and preliminary summarized data for 2021. 2021 data are subject to change and revision prior to the release of the DC SOI.