Read our full report on housing tax expenditures here

This is part two of our four-part blog series highlighting findings from our 2023 Housing Tax Expenditure Review Report. Tax expenditures, also called tax incentives, are preferences in the tax code that convey a benefit to individuals or businesses. In each part of the series, we explain one of the four most significant housing-related tax expenditures in DC and its impact on residents. These four housing tax expenditures are the homestead deduction for real property tax (part 1), property tax assessment increase cap credit, homestead deduction for senior or disabled residents, and the individual income tax credit for Schedule H. In this second post, we focus on the tax credit that caps annual increases in property tax assessments in the District. We look at current credit amounts and number of recipients, the history of the cap, and how the cap benefits people of different incomes, neighborhoods, and lengths of home ownership.

The Assessment Increase Cap Credit:

District homeowners who qualify for the homestead deduction (those whose DC home is their principal residence and who successfully applied to the program) are automatically eligible for an annual assessment increase cap credit. The credit limits the taxable assessed value increase to 10 percent each year. Furthermore, for those who qualify for the senior or disabled resident homestead deduction, the cap is 2 percent.

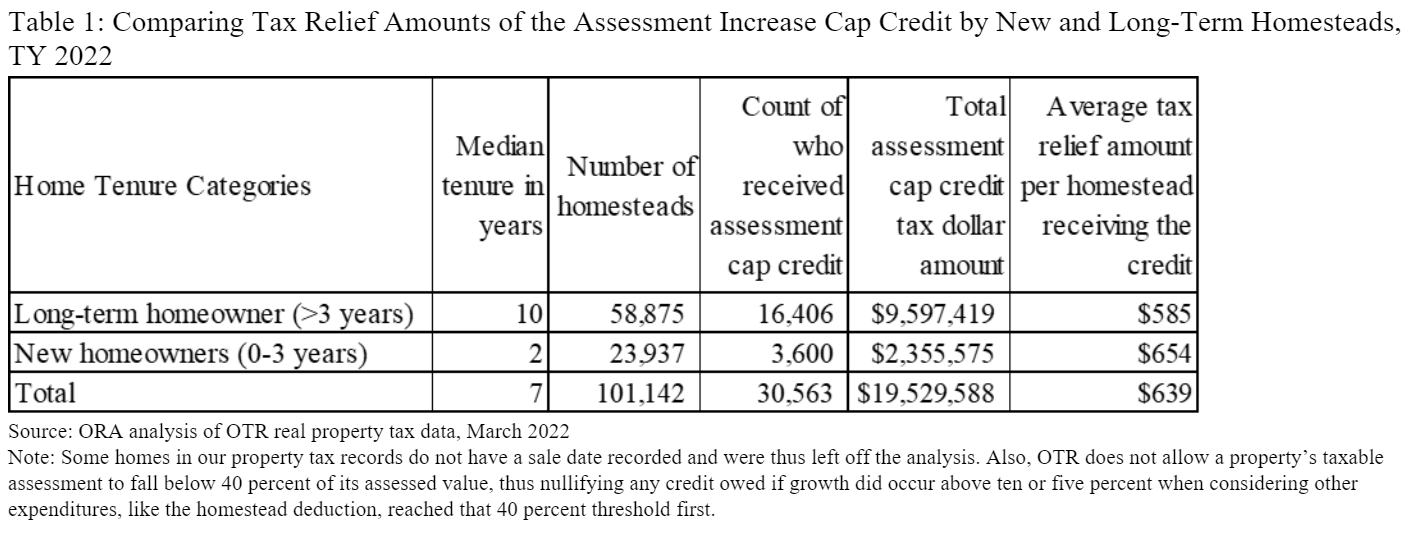

In the tax year 2022, 30 percent, or 30,563 out of the 101,142 active homesteads in DC, received property tax relief. The average tax relief per homestead that benefited from the cap credit was $639. However, most of the total relief went to long-term homesteaders, as shown in Table 1. The total forgone revenue from the program in tax year 2022 was approximately $19.53 million. It is worth noting that this total has progressively decreased every year since tax year 2017 and has not been this low since before our analysis period.

How we got here:

When the assessment increase cap credit was enacted in 2001, interest in moving to the District and its housing market had re-intensified, pushing demand for city services and existing home values to levels not yet seen. The DC government was also changing its property assessment process from once every three years to once a year. This move brought many undervalued properties in line with current market values due to the delay in reassessments. The assessment growth cap was intended to buffer the impact of the transition on residents’ property tax bills. The cap was set at 25 percent in 2001. As the Council committee report outlined, the program was meant to blunt the “sticker shock” of homeowners' assessment increases and subsequent property taxes.1 As the same committee report noted, the initial 25 percent cap did not do enough to blunt the rapid increase in homeowners’ taxable value. The cap was lowered to 10 percent in 2006, and in 2019 a special category was created for senior or disabled with a cap of 5 percent, which was reduced to 2 percent in 2023. The motivation behind the larger tax relief percentage for this special group was to create more stable costs in real property taxes for seniors or individuals with disabilities, who are often on fixed incomes.2

Impact of the Assessment Increase Cap Credit:

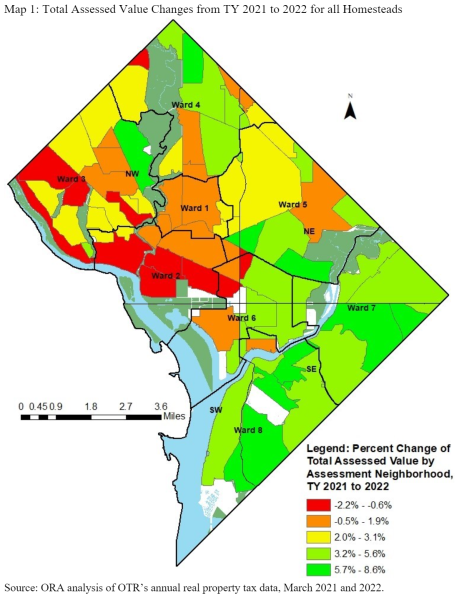

Tax revenue forgone due to the assessment increase cap credit in TY 2022 accounted for 9.2 percent of the total estimated forgone amount for DC’s categorical housing tax expenditures, the smallest of the four analyzed in this category. There has been no increase in the total forgone amount or number of beneficiaries for this expenditure since TY 2017, reflecting the recent slowdown in the growth of residential properties in the District. Conversely, the average tax dollar relief amount has increased recently, perhaps due to housing market dynamics and the new senior and disabled assessment cap credit, which took effect in 2019. The assessment increase cap credit has successfully protected homesteaders from sharp increases in annual property assessments. However, the effectiveness of the protection varies by location and homeowner’s tenure. Map 1 shows that generally, neighborhoods with high growth in assessments from TY 2021 to 2022 tended to be in Wards 5, 7, and 8, while neighborhoods with low growth or declines in assessed values tended to be in Wards 2 and 3. Historically, the cap was especially effective between 2001 and 2007, when the District saw considerable yearly growth in assessments in most neighborhoods, when the cap was higher.

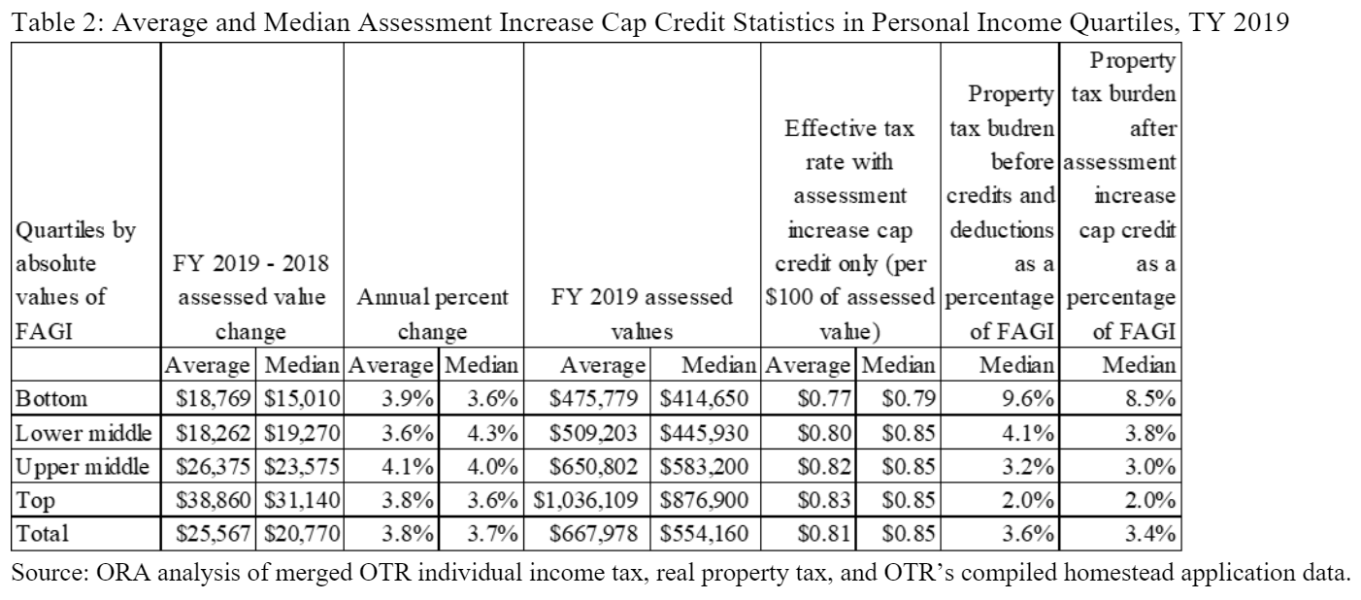

In 2019, those at the lower end of the income and wealth distribution felt the greatest proportion of tax relief. When we combine data from individual income tax returns with real property tax rolls, we find a strong correlation between a taxpayer's income and the value of their property. Table 2 demonstrates that in FY 2019, the property tax burden expressed as a percentage of beneficiaries' federal adjusted gross income, was reduced most by this program for those in the lower half of the income distribution. There are multiple reasons why this program is most beneficial for those in the bottom half of the income distribution. First, lower-assessed valued homes have more room for growth, making it easier for homeowners to see an increase in their home's value. Second, homeowners with lower-assessed valued homes tend to stay in their residences for more extended periods, which means they will benefit from the program's savings for a more extended period. Lastly, the credit amount is proportionally larger for taxpayers with lower incomes, which means they will receive a greater proportional benefit from the program. The distribution of relief is more progressive than previous research indicated and achieves one of its intended goals.

In summary, this tax relief is administratively complex and horizontally inequitable because the tax relief varies with homeowners’ tenure and location and, according to this analysis, is progressive. Its efficiency, that is, whether the District government could provide more benefits with the available revenue, is difficult to determine because of the fluctuations in housing value over the past two decades. Still, it is achieving its legislative intent of moderating sharp growth in property tax bills for homestead beneficiaries who stay in their homes long enough to reap the benefits.

In the next installment of this blog series, we will present and discuss the senior or disabled resident homestead property tax deduction and offer descriptive analyses and visualizations to review its effectiveness against its stated goal.

What is this data?

The sources include real property public extract data (FY 2015-2022), individual income tax return data (FY 2015-2019), and a recently compiled list of approved paper or online homestead applications (FY 1978-2020) from the Office of Tax and Revenue (OTR). Due to the lag in income tax return data availability, income and property tax matching was limited to FY 2019.